What is a balance sheet for a business? What does a balance sheet tell you about a business’s finances that an income sheet can’t?

The balance sheet provides a snapshot of a company’s financial position at a specific time. Karen Berman and Joe Knight explain how balance sheets present your business’s overall value, what kinds of assumptions underlie your balance numbers, and what the balance sheet reveals about your business that a simple income statement cannot.

Continue reading to learn the three main sections of a balance sheet and how to read one.

The Balance Sheet

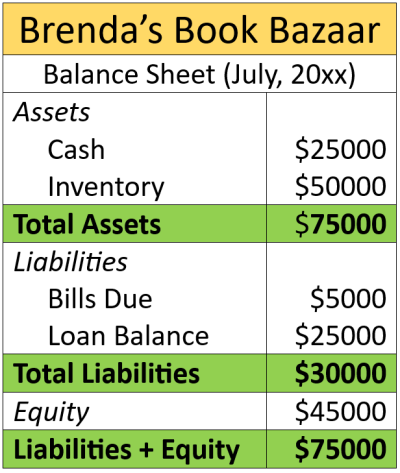

What is a balance sheet for a business? The balance sheet consists of three main sections—assets, liabilities, and how much equity the owners have in the business. The fundamental equation behind the balance sheet states that assets always equal liabilities plus equity. Assets are what the company owns, including cash, equipment, and intangibles like brand names and intellectual property. Liabilities are what the company owes in the form of outstanding debts. Lastly, equity shows what the company’s owners’ stake is worth. To conceptualize this, think of owning a house. Your asset would be the assessed value of your home. Your liability would be the balance left on your mortgage. Your equity, therefore, is the amount left over—how much your ownership of your home is worth.

(Shortform note: Analyzing the balance sheet is the nuts-and-bolts way to calculate a company’s equity, but a short-hand approach used by many investors is based on Efficient Market Theory (EMT)—the proposal that a business’s stock price always reflects its true equity value. According to EMT, all you have to do is take a company’s number of shares and multiply it by the stock price to determine the business’s total equity. Whether this is true has long been debated. In his Essays, investor Warren Buffett argues that EMT is utter nonsense and that a company’s true value—its owners’ equity—can only be achieved by digging through the balance sheet in the way that Berman and Knight describe.)

Many of the line items on the balance sheet involve estimates and judgments similar to those on the income statement. For example, whatever methods you use to place value on unsold inventory, depreciate your assets, and estimate payments on outstanding debt will all require assumptions that can significantly impact the numbers. Berman and Knight warn that faulty assumptions can lead to bad decisions or even to disaster, as seen during the 2008 financial crisis with mortgage-backed securities.

(Shortform note: In The Big Short, Michael Lewis details the financial crisis that Berman and Knight use as an example of assumptions gone wrong. In this case, Wall Street financial institutions made the faulty assumption that mortgage-backed securities—bonds that used bundles of home loans to generate revenue—were stable financial instruments that would pay off for investors. This proved dramatically not to be the case. In 2007, when the actual value of the underlying loans began to plummet below Wall Street’s assumptions, every bank and brokerage that listed these bonds as a balance sheet asset saw their equity plummet as well, triggering the financial meltdown that took place the following year.)

Reading the Balance Sheet

While managers often focus primarily on the income statement, Berman and Knight say that investors and financial professionals tend to examine the balance sheet first. This is because the balance sheet reveals important information about your company’s solvency and overall financial health. For instance, someone interested in buying stock in your business might look at your balance sheet’s equity line, divide that amount by the number of shares, and decide if your stock is priced too high or low. They might also look at how much outstanding debt you have to judge if your business has overleveraged itself to the point that it might risk insolvency during an economic downturn.

(Shortform note: The balance sheet analysis that Berman and Knight describe is the strategy Warren Buffett used to make his first fortune. In The Snowball, biographer Alice Schroeder writes that Buffett would invest in companies that the stock market valued so low that the stock price was less than the equity it represented. These were not healthy companies, but their assets could be sold off at a profit compared to the stock price Buffett paid to acquire them. Buffett’s cardinal rule, however, was to avoid using debt to finance business acquisitions. It was easy access to debt that drove the corporate takeover craze in the 1980s and the subsequent crash in the 1990s, which Buffett personally stepped in to help mitigate.)

Berman and Knight are careful to be clear that the balance sheet doesn’t exist in isolation, but is closely linked to other financial statements. Every change to the income statement impacts the balance sheet in some way. For instance, an uptick in income often increases owners’ equity, while selling products at a discount may decrease total assets. Understanding these connections helps you see how your decisions might affect your company’s overall financial position beyond what’s recorded on your income statement alone.

(Shortform note: One tactic to adjust the income and balance sheets that’s become prevalent in Hollywood is to cancel nearly completed films and take the loss as a write-off. Berman and Knight discuss write-offs as a necessary hardship when a business project fails, but movie studios such as Warner Brothers have canceled several much-anticipated films to boost their financial position. If a completed project is taken off the books, then its expenses no longer show on the income statement, increasing overall estimated profit, nor will the film’s projected marketing budget appear as a liability on the balance sheet. The downside, of course, is that moviegoers will never see Coyote vs. Acme, despite the film’s acclaim from early screenings.)