What’s an income statement in business? How does an income statement track revenue?

The first document any business owner needs to understand is the income statement. This shows whether your company is profitable. According to Financial Intelligence by Karen Berman and Joe Knight, an income statement requires careful interpretation.

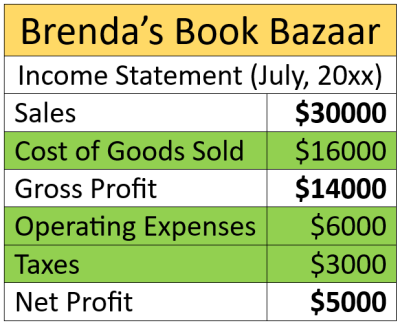

Keep reading to learn what an income statement tells you about your business’s financial health.

The Income Statement

In essence, an income statement in business (also known as a profit-and-loss statement) lists the amount of revenue your company takes in from the goods and services it sells during a specified period. It then subtracts what those goods and services cost to produce, your standard operating expenses, and lastly, your taxes, to show how much profit your business generates. Berman and Knight explain what the income statement shows, how it tracks revenue, and the different ways it can account for expenses.

While this sample income statement may seem straightforward, Berman and Knight insist that many of the numbers on an income statement involve estimates and assumptions by accountants. For example, in the simplified statement above, the amount listed in “sales” may include estimated payments that haven’t been received yet. Understanding those nuances is crucial for managers to accurately assess their company’s performance.

(Shortform note: At the time of Financial Intelligence’s publication, accountants had to interpret data themselves, but today, businesses are turning to artificial intelligence (AI) to make projections and estimates for their income statements. AI can improve a statements’ accuracy by speeding up data analysis, reducing human error and processing large amounts of financial data quickly. AI systems can automatically track transactions and categorize expenses, and by analyzing historical patterns, it can predict future budgeting needs and anticipate revenue. Additionally, AI can help detect fraud and prevent misrepresentations from affecting a business’s income statement.)

One of the trickiest parts of the income statement is determining when and how much revenue to report. Berman and Knight explain that companies can only record revenue when it’s earned, typically when a customer receives a product or service. In some industries, this is simple—you record revenue when someone buys a car part or pays for a haircut. However, in more complicated situations, such as building a factory or providing support for an ongoing government contract, determining exactly when revenue should be recorded on an income statement involves significant judgment—such as whether to report it all at the point of sale or to spread the revenue out over several quarters or years.

(Shortform note: A variation of the rule that Berman and Knight cite above is the “percentage of completion method” of recording revenue for ongoing projects. This method involves reporting revenue on an incremental basis, comparing your current income and expenses to the total estimated costs of a project. To use this method of recording revenue, two conditions must be met—your company’s ability to collect payment must be guaranteed, and your ability to estimate your total costs and when your project will be completed must be reasonably accurate. Businesses that use this accounting method include construction firms, defense contractors, and software development companies with long-term projects.)

Recording Expenses

You also have flexibility in how to report expenses on your income statement. Different expenses may be included in the cost of goods sold or as operating expenses, and the dividing line isn’t always clear. Berman and Knight explain that operating expenses are spread out over time, but the cost of goods sold must be reported in the same period as the revenue from those goods. For instance, in the sample income statement above, the cost of goods can include inventory purchased prior to the month it was sold. How expenses are classified can affect key metrics like gross profit (revenue minus the cost of goods), so shifting an expense from one line to another can impact how profitable a good or service appears on the statement.

(Shortform note: In service industries that don’t sell products, the cost of goods sold is often replaced by the cost of services, also known as the “cost of revenue.” Berman and Knight mention this concept, but they don’t explain how to calculate it. For instance, it may include the wages of employees directly involved in providing a service to your clients, but not wages that aren’t directly tied to the services rendered. Any materials or supplies directly used in providing the service are included, as well as the cost of any subcontractors employed to deliver the service. As with cost of goods sold, any expenses solely incurred to keep the business running are instead listed as operating costs, not cost of services, on the income statement.)

Berman and Knight also discuss noncash expenses, such as depreciation and amortization, that have a major impact on reported profits. Depreciation is the cost of a physical asset, such as a building or a piece of equipment, divided across its projected lifetime. Amortization is the same basic concept, but applied to intangible assets such as patents. Companies have discretion in estimating the useful life of assets and how quickly to depreciate them. If your accountants change depreciation assumptions, such as deciding that a fleet of trucks will last seven years instead of five, that can significantly alter the income statement’s profit line. Therefore, managers should know what assumptions are being used for all their major assets.

(Shortform note: Though businesses can decide how to depreciate assets, in the US they’re legally required to depreciate assets in one way or another. However, how to amortize intangible assets is becoming increasingly complex in the digital age, when those assets can include AI algorithms and software that are constantly changing over time. Berman and Knight’s financial rules still apply, but estimating the useful lifespan of digital intellectual property is tricky. Some argue that since their lifespans are potentially unlimited, digital assets shouldn’t be amortized, but tested regularly to determine if they’re still useful. If not, you can write them off as a loss.)

—Book Overview")

")