This article is an excerpt from the Shortform book guide to "Financial Intelligence" by Karen Berman and Joe Knight. Shortform has the world's best summaries and analyses of books you should be reading.

Like this article? Sign up for a free trial here.

What are the basic financial terms you need to know as a business owner? What’s the difference between an income statement and a cash flow statement?

Understanding your business’s finances requires making sense of different types of reports. Unfortunately, according to Karen Berman and Joe Knight, financial statements aren’t as straightforward as they may seem.

Below, we’ll break down financial literacy for business owners who want to understand their company’s numbers.

Financial Literacy 101

While accounting and finance appear to deal with hard numbers, they actually involve significant judgment calls and estimations by accountants. As part of their discussion on financial literacy for business owners, Berman and Knight explore the three most important documents that reveal the state of a business’s financial health—the income statement, the balance sheet, and the cash flow statement.

For every one of these documents, Berman and Knight argue that financial intelligence means understanding which numbers are well-supported and which ones rely on assumptions. Accounting practices aim to reveal your business’s reality through numbers, but they’re also inherently imprecise. Accountants make many guesses and assumptions when preparing financial statements—for instance, they frequently have to decide where to allocate certain types of expenses or how to estimate the useful lifespan of equipment. Their choices affect the numbers, and knowing that lets you interpret financial reports more accurately.

(Shortform note: Berman and Knight present the traditional approach to accounting used by the majority of businesses today, but in Profit First, Mike Michalowicz criticizes traditional accounting for being so unintuitive that it leads many entrepreneurs to failure. Michalowicz doesn’t argue against traditional accounting’s math, but he states that traditional accounting methods clash with the way most people think and make decisions. In particular, he criticizes traditional accounting’s implied assumptions that profit growth equals success and that profits should always be reinvested in your business. Berman and Knight don’t address these assumptions—their focus is squarely on interpreting the numbers.)

In the US, the standard accounting rules for business are the Generally Accepted Accounting Principles (GAAP), as established by the Financial Accounting Standards Board (FASB). Berman and Knight point out that GAAP rules provide guidelines for financial reporting, but they still allow for personal judgment. Companies have leeway in how they apply GAAP to their specific situations, which means that seemingly objective financial statements will actually reflect many subjective decisions made by accountants and managers.

In addition to GAAP, many companies also use non-GAAP financial measures that sometimes provide a clearer picture of their business performance. However, Berman and Knight state that non-GAAP numbers are not standardized and can be manipulated. Companies can legally use various accounting techniques to make their financial positions look better, and while they’re not strictly fraudulent, these practices significantly alter how a company’s performance appears. Understanding these techniques gives you insight into your business’s true financial position beyond what’s shown on its official statements.

| GAAP and Beyond Berman and Knight aren’t blind to the fact that GAAP accounting guidelines are imperfect. Critics of GAAP cite several shortcomings that can mislead investors, such as GAAP’s reliance on estimates and guesses that can be inaccurate despite accountants’ best intentions. Also, GAAP reporting may not accurately capture the value of innovation in rapidly changing industries. Because of the importance that businesses place on GAAP, managers are often incentivized to manipulate their financial statements to meet financial goals or present a more favorable picture of the company’s performance. These issues make it challenging for business leaders to truly understand a company’s financial health. Though Berman and Knight are correct to point out that non-GAAP reporting is less stringent than GAAP, and is therefore even more subject to manipulation, it does have valid uses. For instance, non-GAAP numbers let companies exclude expenses that don’t reflect ongoing business performance, such as R&D, marketing costs, and non-cash expenses like stock-based CEO compensation. Additionally, one-time costs such as restructuring charges or asset sales can be removed to provide a more accurate forecast of future earnings. Often, non-GAAP reporting lets companies give investors the option to make their own judgments about a business’s profitability based on which factors they consider most relevant. |

The Income Statement

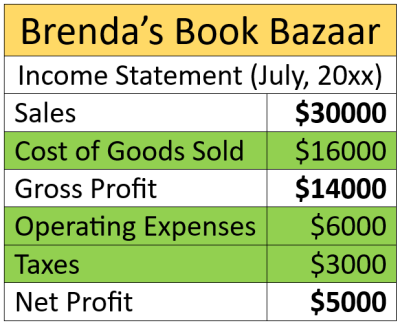

The first statement to understand is your business’s income statement. This is a key financial document that shows whether your company is profitable, but it requires careful interpretation. In essence, the income statement (also known as a profit-and-loss statement) lists the amount of revenue your business takes in from the goods and services it sells during a specified period. It then subtracts what those goods and services cost to produce, your standard operating expenses, and lastly, your taxes, to show how much profit your business generates. Here, we’ll explain what the income statement shows, how it tracks revenue, and the different ways it can account for expenses.

While this sample income statement may seem straightforward, Berman and Knight insist that many of the numbers on an income statement involve estimates and assumptions by accountants. For example, in the simplified statement above, the amount listed in “sales” may include estimated payments that haven’t been received yet. Understanding those nuances is crucial for managers to accurately assess their company’s performance.

One of the trickiest parts of the income statement is determining when and how much revenue to report. Berman and Knight explain that companies can only record revenue when it’s earned, typically when a customer receives a product or service. In some industries, this is simple—you record revenue when someone buys a car part or pays for a haircut. However, in more complicated situations, such as building a factory or providing support for an ongoing government contract, determining exactly when revenue should be recorded on an income statement involves significant judgment—such as whether to report it all at the point of sale or to spread the revenue out over several quarters or years.

The Balance Sheet

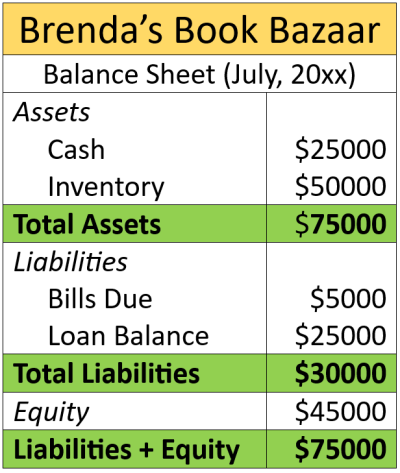

The next critical financial statement to understand is the balance sheet, which provides a snapshot of a company’s financial position at a specific time. Berman and Knight explain how balance sheets present your business’s overall value, what kinds of assumptions underlie your balance numbers, and what the balance sheet reveals about your business that a simple income statement cannot.

The balance sheet consists of three main sections—assets, liabilities, and how much equity the owners have in the business. The fundamental equation behind the balance sheet states that assets always equal liabilities plus equity. Assets are what the company owns, including cash, equipment, and intangibles like brand names and intellectual property. Liabilities are what the company owes in the form of outstanding debts. Lastly, equity shows what the company’s owners’ stake is worth. To conceptualize this, think of owning a house. Your asset would be the assessed value of your home. Your liability would be the balance left on your mortgage. Your equity, therefore, is the amount left over—how much your ownership of your home is worth.

Many of the line items on the balance sheet involve estimates and judgments similar to those on the income statement. For example, whatever methods you use to place value on unsold inventory, depreciate your assets, and estimate payments on outstanding debt will all require assumptions that can significantly impact the numbers. Berman and Knight warn that faulty assumptions can lead to bad decisions or even to disaster, as seen during the 2008 financial crisis with mortgage-backed securities.

The Cash Flow Statement

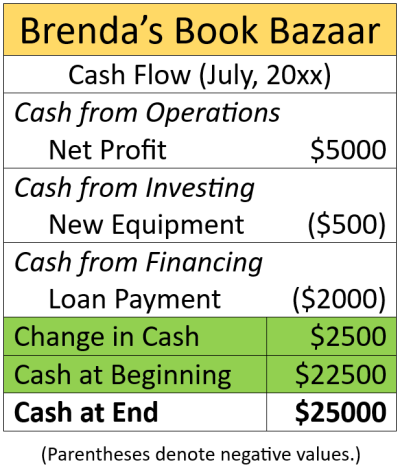

While the income statement and the balance sheet give an overview of a business’s financial position, taking into account past and future revenue and expenses, the cash flow statement fleshes out the full picture of where a business stands in the present—and whether it can afford to pay its bills. We’ll explain how the cash flow statement organizes revenue and expenses, what it can tell you that other statements don’t, and why it’s important to everyone in the business.

The cash flow statement shows how much money is coming in and going out in three different areas of the business:

- Operating cash flow shows how much cash the company spends and generates while performing its core business operations.

- Investing cash flow reveals how much the company is spending on itself in terms of capital assets and investments for the future.

- Financing cash flow shows how much of the business is funded through loans versus shareholder investments.

By examining these three areas, managers can gain insight into the company’s strategy, its ability to fund its own growth, and its reliance on outside capital.

Berman and Knight list several reasons why the cash flow statement provides a clearer picture than profit figures alone, because profit does not equal cash on hand. A company can be profitable on paper but still run out of cash if it can’t collect its debts or if it has large expenses to be paid before its revenue comes in. Also, cash figures aren’t as dependent on potentially faulty accounting estimates as profit figures are. Lastly, knowing how much cash you have helps you decide when to take advantage of business opportunities and tells you how much to hold in reserve so you can weather downturns without relying too heavily on external financing.

Berman and Knight emphasize that all managers impact cash flow, not just those in finance roles. Sales managers influence how quickly customers pay, bringing cash into the business. Operations managers affect inventory spending, which impacts cash flowing out. Therefore, by understanding the cash flow statement, managers can make more informed decisions that improve the company’s financial health and can speak more knowledgeably with executives about the cash implications of various projects and initiatives.

———End of Preview———

Like what you just read? Read the rest of the world's best book summary and analysis of Karen Berman and Joe Knight's "Financial Intelligence" at Shortform.

Here's what you'll find in our full Financial Intelligence summary:

- How you can learn basic financial knowledge, regardless of your background

- How to analyze your company's data using ratios and calculations

- How your balance sheet can help you maximize efficiency

")