This article is an excerpt from the Shortform book guide to "Financial Intelligence" by Karen Berman and Joe Knight. Shortform has the world's best summaries and analyses of books you should be reading.

Like this article? Sign up for a free trial here.

What’s Financial Intelligence by Karen Berman and Joe Knight about? Are you a business owner struggling to understand complex financial statements?

In Financial Intelligence, Karen Berman and Joe Knight argue that basic financial knowledge is something you can learn, regardless of your educational background or your aptitude for numbers. Developing financial intelligence lets you analyze your company’s performance, spot potential issues, and make stronger cases for your business ideas.

Read below for a brief overview of Financial Intelligence.

Overview of Financial Intelligence by Karen Berman & Joe Knight

Understanding accounting can be a daunting challenge for many people who struggle just to balance their bank accounts. Even in the business world, many managers, executives, and entrepreneurs feel their eyes glaze over when presented with the complex financial statements that represent the lifeblood of their companies. Yet, every decision-maker involved in running a business needs to know where their money comes from, how it gets spent, and what danger signs may lie hidden in the numbers. What they need is financial intelligence.

In Financial Intelligence, Karen Berman and Joe Knight define the term as a set of learnable skills that let you understand and effectively use financial information in your business. They argue that financial intelligence is something that anyone can develop, regardless of background or aptitude for numbers. Berman and Knight also argue that financial intelligence is crucial for all employees, not just those in finance roles, since it allows for better decision-making and a deeper understanding of how your business operates.

Berman, who died in 2013, was a respected educator and consultant in the field of business finance and financial literacy. Knight is a prominent figure in business education and consulting, having worked as chief financial officer for Setpoint Systems and having served as a board member for several other companies. Berman and Knight worked together at the Business Literacy Institute, which Berman founded to help nonfinancial professionals understand and use financial information. Berman and Knight coauthored several other books, including Financial Intelligence for HR Professionals and Financial Intelligence for Entrepreneurs.

Accounting Literacy 101

Understanding your business’s finances requires making sense of different types of reports. Unfortunately, financial statements aren’t as straightforward as they may seem. While accounting and finance appear to deal with hard numbers, they actually involve significant judgment calls and estimations by accountants. In this part of the guide, we’ll explore the three most important documents that reveal the state of a business’s financial health—the income statement, the balance sheet, and the cash flow statement.

For every one of these documents, Berman and Knight argue that financial intelligence means understanding which numbers are well-supported and which ones rely on assumptions. Accounting practices aim to reveal your business’s reality through numbers, but they’re also inherently imprecise. Accountants make many guesses and assumptions when preparing financial statements—for instance, they frequently have to decide where to allocate certain types of expenses or how to estimate the useful lifespan of equipment. Their choices affect the numbers, and knowing that lets you interpret financial reports more accurately.

In the US, the standard accounting rules for business are the Generally Accepted Accounting Principles (GAAP), as established by the Financial Accounting Standards Board (FASB). Berman and Knight point out that GAAP rules provide guidelines for financial reporting, but they still allow for personal judgment. Companies have leeway in how they apply GAAP to their specific situations, which means that seemingly objective financial statements will actually reflect many subjective decisions made by accountants and managers.

In addition to GAAP, many companies also use non-GAAP financial measures that sometimes provide a clearer picture of their business performance. However, Berman and Knight state that non-GAAP numbers are not standardized and can be manipulated. Companies can legally use various accounting techniques to make their financial positions look better, and while they’re not strictly fraudulent, these practices significantly alter how a company’s performance appears. Understanding these techniques gives you insight into your business’s true financial position beyond what’s shown on its official statements.

The Income Statement

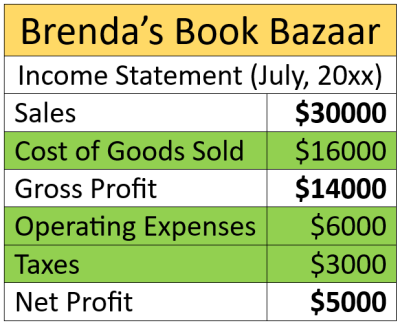

The first statement to understand is your business’s income statement. This is a key financial document that shows whether your company is profitable, but it requires careful interpretation. In essence, the income statement (also known as a profit-and-loss statement) lists the amount of revenue your business takes in from the goods and services it sells during a specified period. It then subtracts what those goods and services cost to produce, your standard operating expenses, and lastly, your taxes, to show how much profit your business generates. Here, we’ll explain what the income statement shows, how it tracks revenue, and the different ways it can account for expenses.

While this sample income statement may seem straightforward, Berman and Knight insist that many of the numbers on an income statement involve estimates and assumptions by accountants. For example, in the simplified statement above, the amount listed in “sales” may include estimated payments that haven’t been received yet. Understanding those nuances is crucial for managers to accurately assess their company’s performance.

One of the trickiest parts of the income statement is determining when and how much revenue to report. Berman and Knight explain that companies can only record revenue when it’s earned, typically when a customer receives a product or service. In some industries, this is simple—you record revenue when someone buys a car part or pays for a haircut. However, in more complicated situations, such as building a factory or providing support for an ongoing government contract, determining exactly when revenue should be recorded on an income statement involves significant judgment—such as whether to report it all at the point of sale, or to spread the revenue out over several quarters or years.

Recording Expenses

You also have flexibility in how to report expenses on your income statement. Different expenses may be included in the cost of goods sold or as operating expenses, and the dividing line isn’t always clear. Berman and Knight explain that operating expenses are spread out over time, but the cost of goods sold must be reported in the same period as the revenue from those goods. For instance, in the sample income statement above, the cost of goods can include inventory purchased prior to the month it was sold. How expenses are classified can affect key metrics like gross profit (revenue minus the cost of goods), so shifting an expense from one line to another can impact how profitable a good or service appears on the statement.

Berman and Knight also discuss noncash expenses, such as depreciation and amortization, that have a major impact on reported profits. Depreciation is the cost of a physical asset, such as a building or a piece of equipment, divided across its projected lifetime. Amortization is the same basic concept, but applied to intangible assets such as patents. Companies have discretion in estimating the useful life of assets and how quickly to depreciate them. If your accountants change depreciation assumptions, such as deciding that a fleet of trucks will last seven years instead of five, that can significantly alter the income statement’s profit line. Therefore, managers should know what assumptions are being used for all their major assets.

The Balance Sheet

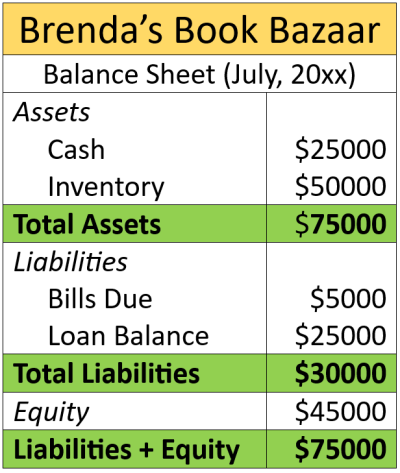

The next critical financial statement to understand is the balance sheet, which provides a snapshot of a company’s financial position at a specific time. Berman and Knight explain how balance sheets present your business’s overall value, what kinds of assumptions underlie your balance numbers, and what the balance sheet reveals about your business that a simple income statement cannot.

The balance sheet consists of three main sections—assets, liabilities, and how much equity the owners have in the business. The fundamental equation behind the balance sheet states that assets always equal liabilities plus equity. Assets are what the company owns, including cash, equipment, and intangibles like brand names and intellectual property. Liabilities are what the company owes in the form of outstanding debts. Lastly, equity shows what the company’s owners’ stake is worth. To conceptualize this, think of owning a house. Your asset would be the assessed value of your home. Your liability would be the balance left on your mortgage. Your equity, therefore, is the amount left over—how much your ownership of your home is worth.

Many of the line items on the balance sheet involve estimates and judgments similar to those on the income statement. For example, whatever methods you use to place value on unsold inventory, depreciate your assets, and estimate payments on outstanding debt will all require assumptions that can significantly impact the numbers. Berman and Knight warn that faulty assumptions can lead to bad decisions or even to disaster, as seen during the 2008 financial crisis with mortgage-backed securities.

Reading the Balance Sheet

While managers often focus primarily on the income statement, Berman and Knight say that investors and financial professionals tend to examine the balance sheet first. This is because the balance sheet reveals important information about your company’s solvency and overall financial health. For instance, someone interested in buying stock in your business might look at your balance sheet’s equity line, divide that amount by the number of shares, and decide if your stock is priced too high or low. They might also look at how much outstanding debt you have to judge if your business has overleveraged itself to the point that it might risk insolvency during an economic downturn.

Berman and Knight are careful to be clear that the balance sheet doesn’t exist in isolation, but is closely linked to other financial statements. Every change to the income statement impacts the balance sheet in some way. For instance, an uptick in income often increases owners’ equity, while selling products at a discount may decrease total assets. Understanding these connections helps you see how your decisions might affect your company’s overall financial position beyond what’s recorded on your income statement alone.

The Cash Flow Statement

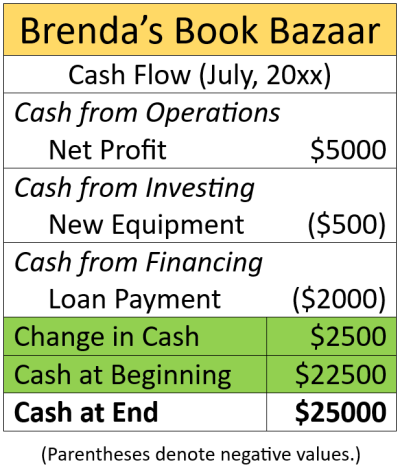

While the income statement and the balance sheet give an overview of a business’s financial position, taking into account past and future revenue and expenses, the cash flow statement fleshes out the full picture of where a business stands in the present—and whether it can afford to pay its bills. We’ll explain how the cash flow statement organizes revenue and expenses, what it can tell you that other statements don’t, and why it’s important to everyone in the business.

The cash flow statement shows how much money is coming in and going out in three different areas of the business:

- Operating cash flow shows how much cash the company spends and generates while performing its core business operations.

- Investing cash flow reveals how much the company is spending on itself in terms of capital assets and investments for the future.

- Financing cash flow shows how much of the business is funded through loans versus shareholder investments.

By examining these three areas, managers can gain insight into the company’s strategy, its ability to fund its own growth, and its reliance on outside capital.

Berman and Knight list several reasons why the cash flow statement provides a clearer picture than profit figures alone, because profit does not equal cash on hand. A company can be profitable on paper but still run out of cash if it can’t collect its debts or if it has large expenses to be paid before its revenue comes in. Also, cash figures aren’t as dependent on potentially faulty accounting estimates as profit figures are. Lastly, knowing how much cash you have helps you decide when to take advantage of business opportunities and tells you how much to hold in reserve so you can weather downturns without relying too heavily on external financing.

Berman and Knight emphasize that all managers impact cash flow, not just those in finance roles. Sales managers influence how quickly customers pay, bringing cash into the business. Operations managers affect inventory spending, which impacts cash flowing out. Therefore, by understanding the cash flow statement, managers can make more informed decisions that improve the company’s financial health and can speak more knowledgeably with executives about the cash implications of various projects and initiatives.

Making Sense of the Numbers

Now that we’ve covered the specific information accountants include on business financial statements, we’ll discuss how to interpret and use that information. We’ll begin with how to calculate important numbers that reflect your business’s profitability, efficiency, and potential to attract investors, with extra focus given to the importance of determining your business’s return on investment. After that, we’ll discuss how to manage your working capital to increase how much cash your business keeps on hand.

Remember, Berman and Knight’s main idea is that financial knowledge isn’t just for accountants. Rather, they argue that improving financial intelligence throughout an organization can significantly boost its performance. When employees at all levels understand their business’s financial aspects, they make better decisions, react more quickly to changes, and contribute more effectively to the company’s success. However, creating a financially intelligent company requires more than just a book or a one-time training session. Instead, financial training should be an ongoing process that’s part of the company’s culture. Training should be customized to your company’s specific needs and include a basic foundation for all employees.

The authors also argue that in today’s business world, where job security can’t be taken for granted, employees have a legitimate interest in understanding their company’s financial health. Berman and Knight advocate for a policy of financial transparency in which financial information is shared widely and explained. They believe this approach can lead to increased trust and loyalty among managers and rank-and-file employees. That being said, public companies must be cautious about sharing non-public information, but the authors maintain that most financial training rarely includes information that would help a company’s rivals.

Important Metrics

To understand which numbers to look at and how to determine what they mean, the authors discuss several key financial ratios that managers, investors, and analysts use to evaluate a company’s performance and financial health. Among all the various financial measures, Berman and Knight identify several important financial measures that indicate a company’s profitability, efficiency, and overall financial strength.

Profitability

To measure a company’s profitability, Berman and Knight offer three financial ratios:

- Gross profit margin: Divide the gross profit number on the income statement by the total sales. This tells you how profitable your products and services are in and of themselves.

- Operating profit margin: First, subtract your operating costs from your gross profit, then divide by total sales. This percentage lets you gauge the profitability of your core business operations.

- Net profit margin: Divide the income statement’s net profit amount by your total sales—this lets you assess your overall profitability after all expenses.

Berman and Knight recommend that you track these ratios over time to spot trends in your company’s profitability. These margins show you how effectively your business generates profits at different stages of the money-making process. For instance, if your gross profit is high but your operating profit is low, then you may be paying too much overhead in day-to-day business operations. With these numbers, you can also compare your performance to business competitors and industry benchmarks.

Efficiency

To measure a business’s efficiency using financial statements, Berman and Knight say to turn to your balance sheet, from which you can assess how well your business is using its resources. For instance, you can measure how quickly you sell your inventory by dividing the average value of the inventory you keep in stock by the cost of goods sold on a daily basis. You can compute how fast customers pay their bills by dividing the amount of money your customers owe by your average daily sales, letting you know how efficient you are at collecting payment for the goods you provide. Finally, you can calculate the turnover rate of all your company’s assets by dividing your total revenue by the value of everything your company owns.

The trick lies in recognizing whether your efficiency numbers are good or bad. Berman and Knight explain that this is largely subjective and changes from industry to industry. Nevertheless, you should track your efficiency numbers over time and compare them to industry standards so you can identify areas for improvement in your business operations. You must also recognize that your efficiency numbers rely heavily on your company’s balance sheet and will reflect any assumptions that you or your accountants make in preparing that document.

Investment Potential

While managers view their businesses from a different perspective than Wall Street investors, Berman and Knight say that it’s important to analyze your financial statements the same way that potential investors will. This is especially crucial if your business wants to finance itself by bringing in shareholders rather than by taking on debt. To make your business more attractive to investors, you need to know what they’re looking for and, if needed, find ways to improve your performance in those areas.

First off, investors expect to see a business’s revenue expand over time. The authors note that sustainable growth rates vary by industry and company size, but consistent growth is key. Another measure investors expect to increase is the amount of earnings per share (EPS), which is the net income on the income statement divided by the company’s total number of shares. This is a metric that investors want to see going up even during economic downturns. Also of value to investors are a company’s ability to generate cash beyond its operating needs and how efficiently a company uses its capital to generate returns for its owners. The latter is reflected in the return on investment (ROI), which we’ll cover in more detail next.

Return on Investment

Perhaps the most basic question anyone who invests in a business asks is, “Will this be a good use of my time and money?” In the simplest terms, the ROI answers this by measuring how profitable an investment is compared to its cost. Berman and Knight discuss how ROI calculations involve estimating future business performance, whether an investment will earn back its value, and what the minimum return must be in order for a business or an investment to move forward.

To calculate ROI, you estimate the initial cash outlay for a business project and project its future cash flows. According to Berman and Knight, the hard part is to make realistic estimates of how much cash your business will generate, not just theoretical profits. Since determining a return on investment involves making guesses as to future performance, calculating the ROI requires significant judgment and estimation, making it as much an art as a science. However, ROI calculations are useful beyond measuring the performance of your business as a whole—they can also be applied to any new project or venture you create within the larger organization, such as investing in a new product or service.

When calculating your return on investment, it’s also common to take into account how quickly your investment will pay off. The simplest way to do this is to calculate how long it will take for an investment to recoup its initial costs. While easy to understand, this approach has limitations, since it doesn’t consider how money’s value changes over time or what happens after the payback period. Berman and Knight prefer a calculation method called net present value (NPV), which is more complex but provides a more comprehensive analysis. In short, the NPV takes into account that due to inflation, money in the future is worth less than the same amount of money today.

To determine if your ROI is high enough, Berman and Knight say you have to decide on your required rate of return. This is the bare minimum amount of return that your business or a shareholder expects to earn back from an investment for it to be worthwhile. Companies set this rate based on factors such as how much risk is involved and what the potential returns are from other potential investments. If a business or a project’s projected rate of return exceeds this benchmark, it’s considered financially attractive. The rate may vary for different industries or economic conditions, reflecting investors’ tolerance for risk and what your financial goals are.

Managing Capital

Since many of the financial tools listed in this guide rely on guesses and assumptions, it’s not hard to imagine how a business might paint a rosy picture of itself by tweaking an assumption here or there. However, Berman and Knight describe a way of using financial numbers to help your company improve its actual performance without increasing sales or bringing costs down. You can do this by managing your working capital—the readily available resources, not theoretical or tied up in long-term debt—by adjusting the timing of how payments are made and carefully controlling inventory levels.

A business’s working capital consists primarily of cash, inventory, and incoming payments, minus short-term liabilities. By effectively managing how it handles capital, your company can free up cash and improve its financial flexibility. Two key metrics that Berman and Knight say to watch are the time it takes to collect on payments, and how long you take to pay your own bills. In general, you want to collect incoming payments as early as possible, while putting off outgoing payments as long as you can without angering your vendors. Doing so maximizes how much cash you have on hand at any moment, even without increasing your sales or bringing down your operating expenses.

Berman and Knight also stress that inventory management is crucial in freeing up cash. While keeping goods and materials in inventory is necessary for many industries, excess inventory ties up cash that could be used elsewhere. The challenge is to maintain enough inventory to satisfy your customers while minimizing the amount of cash it ties up. Managers throughout your company can impact inventory levels, from salespeople placing orders to engineers requesting raw materials, so everyone in the product chain needs to know how they add to or subtract from working capital.

Berman and Knight conclude that even small improvements in capital and inventory management can result in more cash for your business, so a little financial intelligence can go a long way toward your company’s success.

———End of Preview———

Like what you just read? Read the rest of the world's best book summary and analysis of Karen Berman and Joe Knight's "Financial Intelligence" at Shortform.

Here's what you'll find in our full Financial Intelligence summary:

- How you can learn basic financial knowledge, regardless of your background

- How to analyze your company's data using ratios and calculations

- How your balance sheet can help you maximize efficiency