What are the three main areas of cash flow for small businesses? What does a cash flow statement tell you that an income and balance sheet statement don’t?

The income statement and the balance sheet give an overview of a business’s financial position, taking into account past and future revenue and expenses. On the other hand, the cash flow statement fleshes out the full picture of where a business stands in the present—and whether it can afford to pay its bills.

Let’s look at how to interpret a cash flow statement.

The Cash Flow Statement

Karen Berman and Joe Knight discuss cash flow for small businesses, explaining how the cash flow statement organizes revenue and expenses, what it can tell you that other statements don’t, and why it’s important to everyone in the business.

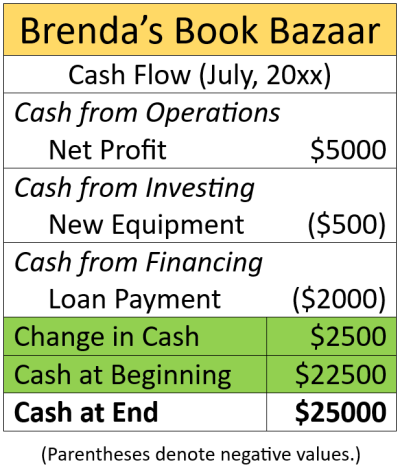

The statement shows how much money is coming in and going out in three different areas:

- Operating cash flow shows how much cash the company spends and generates while performing its core business operations.

- Investing cash flow reveals how much the company is spending on itself in terms of capital assets and investments for the future.

- Financing cash flow shows how much of the business is funded through loans versus shareholder investments.

By examining these three areas, managers can gain insight into the company’s strategy, its ability to fund its own growth, and its reliance on outside capital.

| Personal Cash Flow The three types of cash flow that Berman and Knight illustrate are loosely analogous to the forms of income generation and expenses you may have in your personal life. In Rich Dad’s Cashflow Quadrant, Robert T. Kiyosaki details four types of income streams you can develop both in your career and outside it. Though Kiyosaki focuses on earning cash through different channels, each of his methods has associated expenses that you must also take into account, just as a business does on its cash flow statement. Kiyosaki’s first avenue for cash is the simplest—if you’re an employee, you’re paid for your work. This income, plus its associated expenses, such as work clothes and transportation, constitute your personal operating cash flow. This income stream has the advantage of predictability, but steady employment lacks the sense of security that it provided in generations past. Like a business that coasts on standard operations, this cash flow stream leaves you vulnerable to changes in your market or field. The next option Kiyosaki presents is to be a business owner, in which you invest the time, labor, and costs to form a working enterprise and reap the benefits yourself. This is the personal equivalent of the investing cash flow Berman and Knight describe—just as a business invests in its growth, you can invest in yourself as a business. This cash stream has the disadvantage of being high-risk and high-cost, but it also has a higher potential for reward. Lastly, you have your financing cash flow. On a personal level, this would include the interest paid on the loans, mortgages, and credit cards you use to fund your day-to-day life. However, from Kiyosaki’s point of view, it would also include any wealth you generate as an investor in passive income streams. These include stocks and bonds, as well as income earned from investment properties and other avenues that don’t require your day-to-day attention. If you wished, you could conceivably create a personal cash flow statement similar to that which Berman and Knight illustrate for business use. |

Berman and Knight list several reasons why the cash flow statement provides a clearer picture than profit figures alone, because profit does not equal cash on hand. A company can be profitable on paper but still run out of cash if it can’t collect its debts or if it has large expenses to be paid before its revenue comes in. Also, cash figures aren’t as dependent on potentially faulty accounting estimates as profit figures are. Lastly, knowing how much cash you have helps you decide when to take advantage of business opportunities and tells you how much to hold in reserve so you can weather downturns without relying too heavily on external financing.

(Shortform note: Berman and Knight don’t specify how much cash your business should keep on hand. However, in Great by Choice, Jim Collins and Morten T. Hansen suggest that to survive unexpected fiscal shocks, you should carry three to 10 times the ratio of cash to assets that other companies in your industry maintain. It may seem that having so much idle cash isn’t a good use of a company’s resources, but disruptive economic events are inevitable, and having cash on hand serves as a shock absorber, increasing your company’s chances of survival.)

Berman and Knight emphasize that all managers impact cash flow, not just those in finance roles. Sales managers influence how quickly customers pay, bringing cash into the business. Operations managers affect inventory spending, which impacts cash flowing out. Therefore, by understanding the cash flow statement, managers can make more informed decisions that improve the company’s financial health and can speak more knowledgeably with executives about the cash implications of various projects and initiatives.

(Shortform note: Making all managers money-conscious, as Berman and Knight suggest, is one way to keep them in alignment with your business’s overall goals. In The Essential Drucker, management expert Peter F. Drucker says that people who make management decisions now comprise more than a third of the workforce, and every one of these people is responsible for whether their businesses’ efforts produce their desired effects. In your business, therefore, you should make sure that you and your fellow managers keep their monetary goals in mind, and not just the goals of their departments, teams, or projects.)